Written by Manjunatha Thyagaraj, founder of Relific.io and a leading voice on technology-driven impact measurement.

TL;dR

The evolution of Corporate Social Responsibility (CSR) marks a worldwide shift from optional charitable giving (1950s) to required, quantifiable impact systems (2010s+). In India, this progression was distinctly fast-tracked through the Companies Act 2013, which mandated 2% of net profits for social programs, generating ₹1.27 trillion since 2014, positioning India as the world’s sole nation with a legally binding CSR framework.

- Philanthropic Phase (1950s–1970s): Optional giving and building public goodwill.

- Ethical Phase (1980s–1990s): Accountability to stakeholders and community engagement.

- Strategic Phase (2000s–2010s): CSR merged with business goals (“Creating Shared Value” approach).

- Sustainable/ESG Phase (2020s+): CSR merged with business goals (“Creating Shared Value” approach).

India’s trajectory is uniquely anchored by: Ancient Dāna tradition → Gandhi’s Trusteeship Model → Tata’s institutional philanthropy → 2013 Legal Mandate → 2021 Accountability Amendment → CSR 3.0 (AI-driven impact measurement)

India has achieved what no other nation has attempted: transforming corporate social responsibility from voluntary charity into a legal mandate that has mobilised ₹1.27 trillion ($15.2 billion) since 2014. This transformation journey, from ancient Dāna traditions to AI-powered impact measurement, positions India as a global pioneer in structured corporate giving.

Key Takeaways:

- ₹1.27 trillion mobilised through mandatory CSR since 2014

- 20,000+ companies now contribute to social development

- World’s only country with legally enforceable CSR spending

- CSR spending increased by 1.5 times in eight years

- Evolution from CSR 1.0 (Compliance) → CSR 2.0 (Accountability) → CSR 3.0 (ESG Integration).

- The CSR law amendment 2021 was a watershed moment, shifting focus from spending to measurable impact.

As the founder of Relific and architect of an enterprise-grade social impact measurement platform, I’ve observed firsthand that India’s CSR mandate isn’t just legislation, it’s a blueprint for how developing nations can harness corporate resources for sustainable development while maintaining business growth.

In this guide :

- What is the evolution of CSR globally and in India?

- Who is the founder/father of CSR in India?

- What are the phases of CSR evolution?

- How did India’s 2013 law and 2021 amendments reshape corporate responsibility?

- CSR 3.0, ESG integration, and tech-driven impact

1. The Evolution of CSR: A Global Journey from Charity to Strategic ESG

The formal idea of Corporate Social Responsibility (CSR) emerged in 1953 through American economist Howard Bowen’s groundbreaking book, “Social Responsibilities of the Businessman.” Yet, the ethical foundations of businesses wrestling with their duties trace back to the Industrial Revolution. CSR is officially described as the pledge by companies to support sustainable economic growth while enhancing the quality of life for workers, communities, and society as a whole.

1.1 What are the phases of Global CSR Evolution?

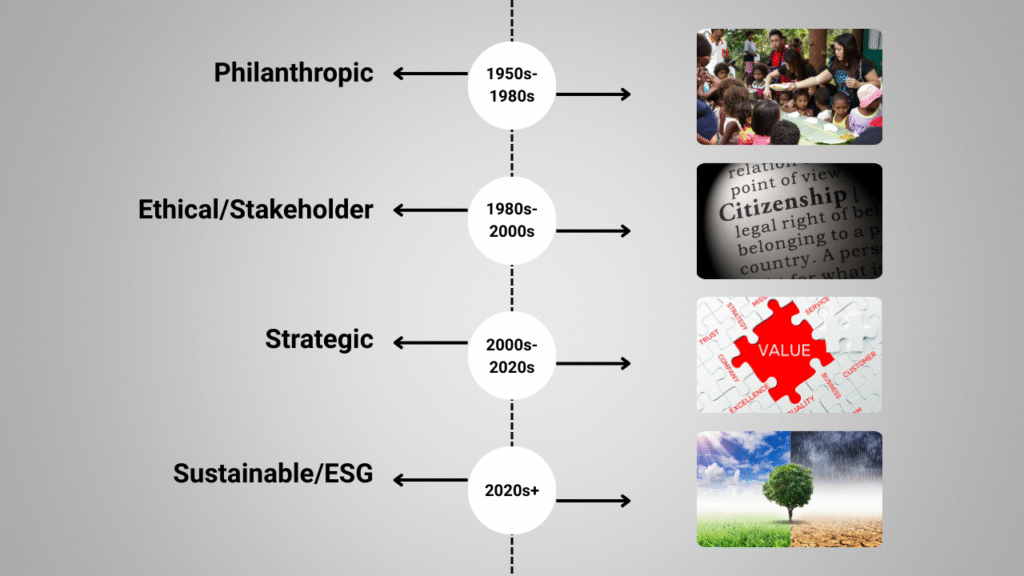

The evolution of Corporate Social Responsibility (CSR) represents a fundamental shift from simple, voluntary charity to mandatory, measurable, and integrated social and environmental strategies. This journey reflects a multi-decade evolution in mindset, progressing through Philanthropic, Ethical, Strategic, and ultimately Sustainable/ESG phases.

Four Global Phases of Evolution

| Phase | Period | Focus | Measurement |

| Philanthropic | 1950s-1980s | Charity, community donations | Anecdotal |

| Ethical/Stakeholder | 1980s-2000s | Corporate citizenship | Qualitative reports |

| Strategic | 2000s-2020s | Shared value creation | KPIs, sustainability reports |

| Sustainable/ESG | 2020s+ | Climate action, governance | ESG scores, SROI, SDG alignment |

1.2 CSR vs. ESG: The Key Distinction for Modern Accountability

The movement into the 2020s has been fueled by market demands for corporate openness, triggering the rise of the Environmental, Social, and Governance (ESG) framework.

- CSR is generally viewed as qualitative and voluntary, focused on reputation and a company’s internal values (e.g., supporting a local school).

- ESG is quantifiable and strategic, prioritising long-term sustainability and financial value creation (e.g., monitoring carbon emissions, pay equity). Investors use ESG scores to assess a company’s strength and future performance, effectively making investor capital the main driver pushing accountability across the globe.

Globally, this change was “pull-driven” by investors requiring transparency. In India, it was “push-driven” through legislation, a crucial difference that makes India’s approach different and strong. While nations in the EU have required ESG disclosure, India stands as a trailblazer in requiring ESG investment.

2. How Did CSR Evolve in India? A Complete History

The global movement towards accountability has been largely “pull-driven” by investor demands and market dynamics requiring openness. This has resulted in regulations like the “EU’s Directive on Non-Financial Reporting (NFRD)”, which requires that large corporations disclose their social and environmental impact.

The development of CSR in India differs from that in the West because it was grounded in longstanding cultural and philosophical traditions well before any corporate legislation existed. This homegrown foundation established a moral obligation that paved the way for the subsequent legal requirement.

India’s strategy is fundamentally different and more proactive. The “Companies Act, 2013” established a “push-driven” framework, making India the first and only major economy to require CSR spending legally. While other countries emphasise disclosure, India’s law mandates financial contribution, making its approach a distinctive and closely monitored experiment in channelling corporate resources for national development objectives.

2.1 The Ancient Blueprint: Dāna and the Moral Imperative

The origins of Indian Corporate Social Responsibility reach back centuries to the cultural practice of Dāna (selfless giving) and Utsarga (charity for community welfare). This philosophy instilled the moral duty for shared responsibility in Indian society thousands of years before modern corporate structures, establishing a natural foundation for CSR implementation.

These traditions funded:

- Public wells and water systems

- Educational institutions (pathshalas)

- Rest houses for travellers (dharamshalas)

- Healthcare facilities (aushadhalaya)

This cultural foundation created fertile ground for modern CSR adoption, distinguishing India’s approach from Western models.

Philosophical Foundation:

- Vedic texts emphasised wealth as a means to serve society

- Buddhist and Jain traditions elevated charitable giving to spiritual merit

- The Bhakti movement democratized philanthropy beyond elites

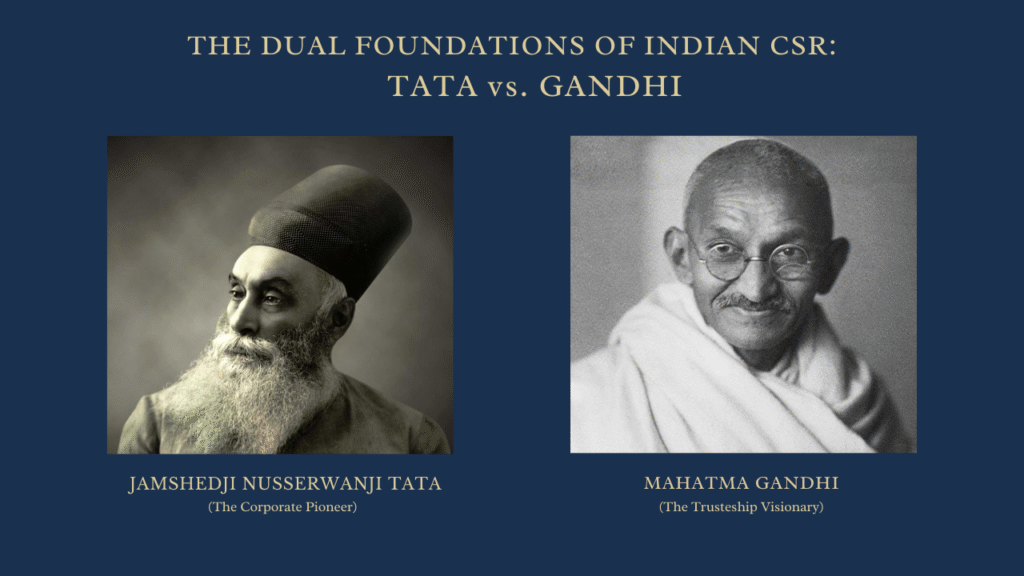

2.2 Who is the Founder of CSR in India? Tatas vs. Mahatma Gandhi

amshedji Nusserwanji Tata is the pioneer and founder of institutionalised CSR in India through the Tata Group. However, Mahatma Gandhi is considered the Philosophical Father whose Trusteeship Model provided the definitive moral framework for industrial giving.

2.2.1 Jamshedji Tata: The Architect of Corporate Giving (1868–1904)

The Tata Philosophy was built on the belief that “what comes from the people should be returned to the people many times over.” This dedication is demonstrated by the fact that 66% of Tata Sons’ equity is owned by charitable trusts, making social contribution a core element of the corporate identity and a trailblazing model of responsible business practices in India.

2.2.2 Mahatma Gandhi: The Philosophical Father (Trusteeship Model, 1940s)

Gandhi believed that business owners are simply custodians of wealth, managing it for society’s benefit rather than personal enrichment. This deeply influenced the conscience of major industrial families, like the Tatas and Birlas, establishing the foundation for the moral acceptance of compulsory contribution decades later.

“I desire to end capitalism almost, if not quite, as much as the most advanced socialist. But our methods differ. My theory of trusteeship is no make-shift, certainly no camouflage.” – Mahatma Gandhi

2.3 The License Raj and Token CSR (1947–1991)

Why did CSR remain rudimentary after India’s independence? During the era of the License Raj (1947–1991), heavy state control and limited private sector autonomy meant that CSR was mostly limited to government-mandated community and labour welfare. With little competitive pressure or global exposure, CSR remained rudimentary:

- It was largely donation-based and unstructured.

- The focus was on corporate survival and basic compliance, rather than strategic social investment.

- Innovation was minimal, and social activities were often driven by the personal relationships of promoters.

During the License Raj era, India’s CSR landscape was bifurcated: PSUs practised state-mandated social welfare as part of their mission, while private companies engaged in token CSR primarily for regulatory compliance and maintaining government relations.

2.3.1 The Role of Public Sector Undertakings (PSUs) (1947-1991)

Following India’s independence and during the License Raj era, extensive state regulation meant that private sector expansion was constrained. During this time, “Public Sector Undertakings (PSUs)” became the main champions of organised CSR.

Companies like ONGC, SAIL, and BHEL had allocated budgets and systems for social development, shaped by government guidelines. Their emphasis was primarily on community upliftment in regions near their facilities, worker welfare, and environmental stewardship.

This historical background is crucial; it demonstrates that the 2013 law didn’t create CSR in India but instead broadened and formalised a practice that was already deeply embedded within the public sector.

2.4 The 1990s Watershed: Globalisation and Professionalisation

The economic liberalisation of 1991 introduced Indian companies to global best practices and international investor attention, driving a transition from simple philanthropy to corporate citizenship and multi-stakeholder responsibility.

The 1990s marked the professionalisation of CSR in India, a pivot from ad-hoc charity to structured, transparent, and accountable social investment. Key pioneers in this shift included:

- Infosys Foundation (1996): Founded by Sudha Murty, this model focused on scalable impact (e.g., libraries, healthcare infrastructure) with transparent reporting, pioneering the “tech company as social investor” model.

- CII-ITC Centre of Excellence for Sustainable Development: Helped professionalise the sector by creating platforms for sharing best practices and promoting standardised reporting.

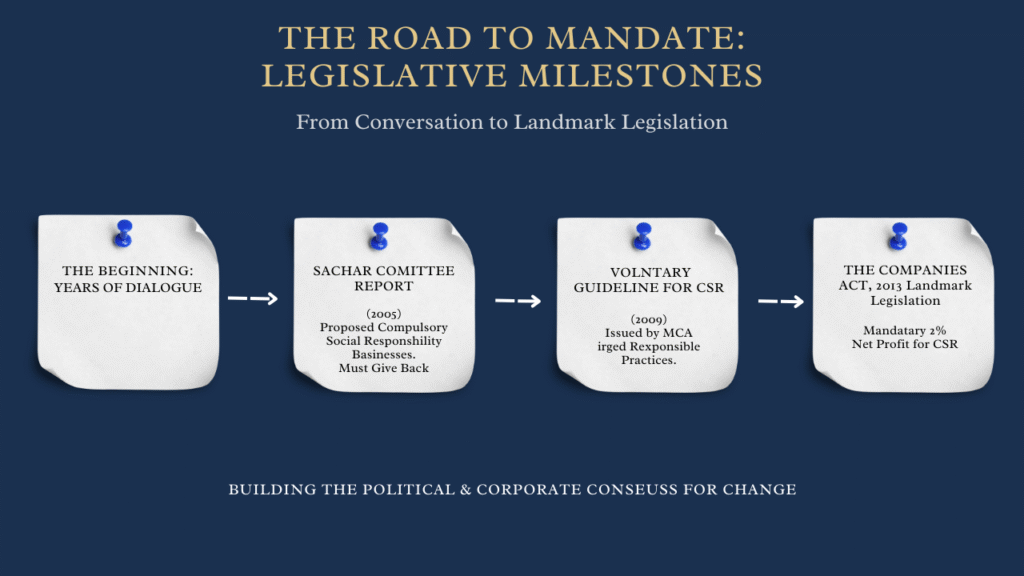

3. The Road to Mandate: Legislative Milestones

he CSR law in India didn’t just materialise in 2013; it was the culmination of years of conversation, advocacy, and careful policy work. Two pivotal moments set the stage for this landmark legislation:

- The Sachar Committee Report (2005): This senior government committee was among the first to officially propose that corporate entities should have a compulsory social responsibility, arguing that businesses gain from society and must give back.

- Voluntary Guidelines for CSR (2009): The Ministry of Corporate Affairs (MCA) issued the first set of voluntary guidelines, encouraging businesses to adopt socially responsible practices and disclose them. These guidelines acted as a precursor, familiarizing the corporate sector with principles that would later be codified into law.

These steps built the political and corporate consensus needed for the groundbreaking legislation that would follow.

4. Section 135: India’s Mandatory CSR Law (The 2% Mandate)

4.1 What is the core requirement of India’s mandatory CSR law?

On April 1, 2014, India did something revolutionary that no other country had done before. With the revised Companies Act, it turned corporate social responsibility from a voluntary act of charity into a legal requirement. Suddenly, businesses weren’t just encouraged to give back, they were required to. This single law triggered a deep and rapid change. It fundamentally reshaped the relationship between Indian companies and the communities around them.

The mandate of Section 135 requires companies meeting specific financial thresholds to spend a minimum amount on social activities:

| Requirement | Condition | Mandate |

| Who Must Comply? | Net Worth ≥ ₹500 crore, OR Turnover ≥ ₹1,000 crore, OR Net Profit ≥ ₹5 crore. | |

| How Much Must Be Spent? | At least 2% of the average net profits of the preceding three financial years. | |

| Where Can It Be Spent? | Only on activities listed under Schedule VII |

4.2 Schedule VII, Permissible CSR Activities

Schedule VII defines where CSR funds can be spent:

- Eradicating poverty and malnutrition

- Promoting education and vocational skills

- Gender equality and women’s empowerment

- Healthcare, including preventive healthcare

- Environmental sustainability

- Protection of national heritage

- Rural development projects

- Technology incubators

- Disaster relief, including COVID-19 relief

4.3 CSR in India: By The Numbers (The Impact of the Mandate)

The immediate impact of India’s CSR law is quantifiable. Since its inception, the law has successfully mobilised massive funds for development:

- 3.5x growth: Increase in CSR spending since the mandate inception.

- 20,000+ companies: Eligible under Section 135.

- Top Contributors (53% of total): Oil/Gas, BFSI, and IT sectors.

- 16% year-on-year growth: FY24 CSR spending reached ₹17,967 crore vs ₹15,524 crore in FY23.

- ₹10,085 crore: Allocated to the education sector, the highest among all focus areas.

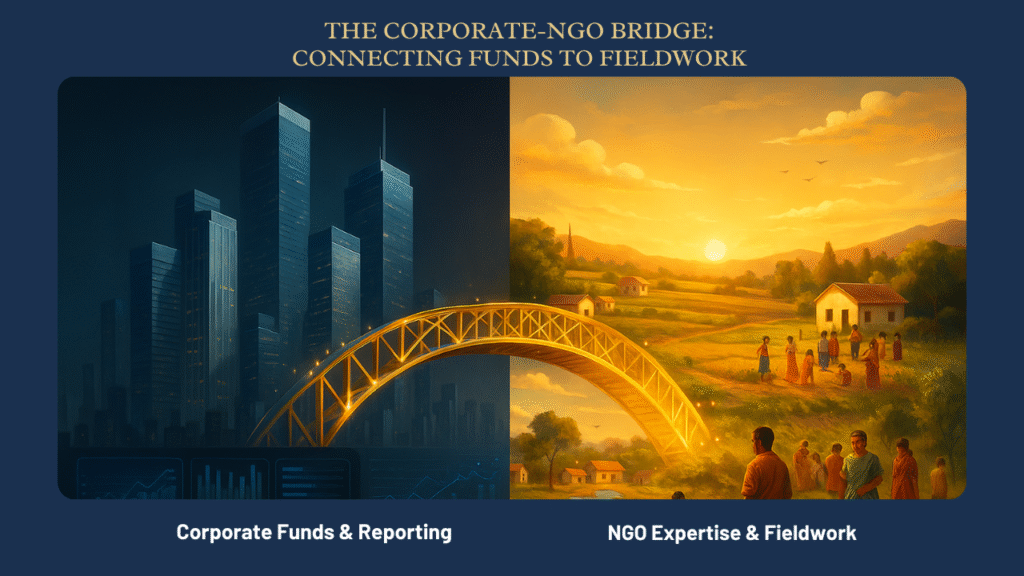

4.4 The Crucial Role of Implementation Agencies (NGOs)

It’s important to understand that companies rarely execute CSR projects on the ground themselves. The mobilised funds are channelled through implementation partners, typically non-governmental organisations (NGOs), trusts, and Section 8 companies. This corporate-NGO partnership is the backbone of the Indian CSR ecosystem. However, it brings its own set of challenges:

- Due Diligence: Companies need to make sure their partners are properly registered with the MCA (through Form CSR-1) and can actually deliver what they promise, not just sound good on paper.

- Capacity Building: Many NGOs are experts in their communities; they know the people, the problems, and the ground realities inside out. But corporate-style reporting and data management is the field where they often struggle. There’s a real gap between their on-ground expertise and what funders expect to see in reports and dashboards.

- Strategic Alignment: The magic happens when companies and NGOs work as genuine partners, not just in a client-vendor arrangement where one writes checks and the other sends reports.

4.5 Sectoral Allocation Breakdown:

| Sector | Percentage of Total Spending |

| Education & Livelihood Development | 44% |

| Healthcare & Sanitation | 29% |

| Rural Development | 7% (A recognised critical gap) |

| Environmental Sustainability | 6% |

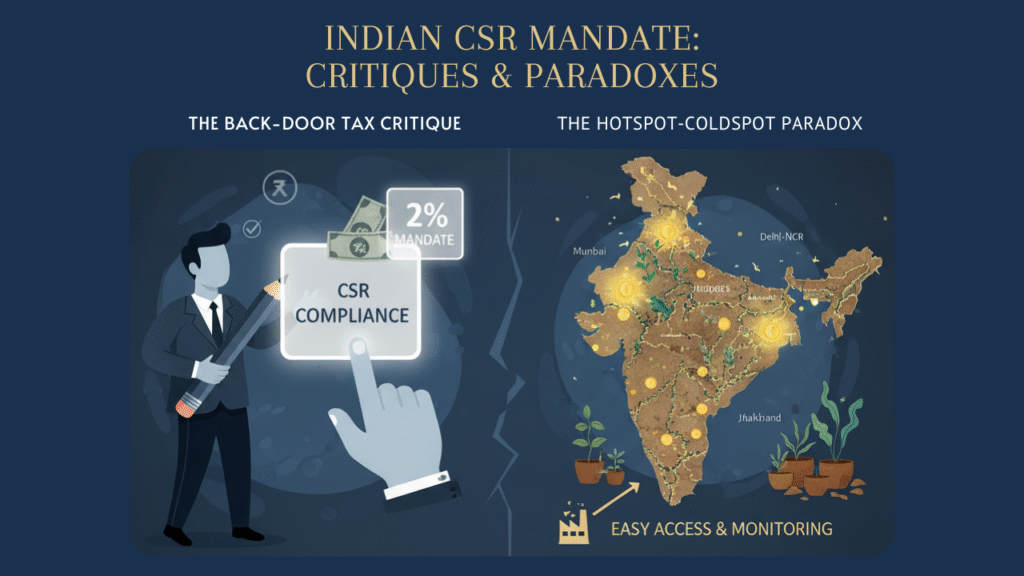

4.6 The Challenges: Back-Door Tax and The Hotspot-Coldspot Paradox

The mandate, while successful in fund mobilisation, has faced two primary criticisms that highlight its limitations:

- The Back-Door Tax Critique

Philanthropists like Azim Premji argue that the mandate is merely a “back-door way to increase corporate taxes.” This shifts the focus from authentic, high-impact philanthropic activity to a “checking the box” compliance mindset, potentially crowding out voluntary, strategic social investment.

Proponents counter that it ensures ₹1.27 trillion is deployed and democratizes contributions beyond a few large conglomerates. The law ensures spending where ethics might otherwise fall short. - The Hotspot-Coldspot Paradox: Here’s the frustrating part, companies are spending big money, but it’s all going to the same places. Cities like Mumbai and Delhi-NCR are soaking up 62% of the funds, while the areas that actually need it most, rural regions, the Northeastern states, places like Jharkhand, are barely getting a look-in. It’s like watering the plants that are already thriving while the ones actually struggling are being ignored.

The Root Cause: Section 135 instructs companies to spend, but it doesn’t say where. So what happens? Companies go for the low-hanging fruit places they can easily get to, easily keep tabs on, and easily manage. It just makes sense from their perspective.

The Reality:

Neither perspective is entirely wrong. CSR has long been characterized by a push-and-pull between compliance and genuine commitment. Recognizing this tension, the government intervened with the 2021 amendment, making it clear that CSR is no longer just about spending—it must demonstrate meaningful impact.

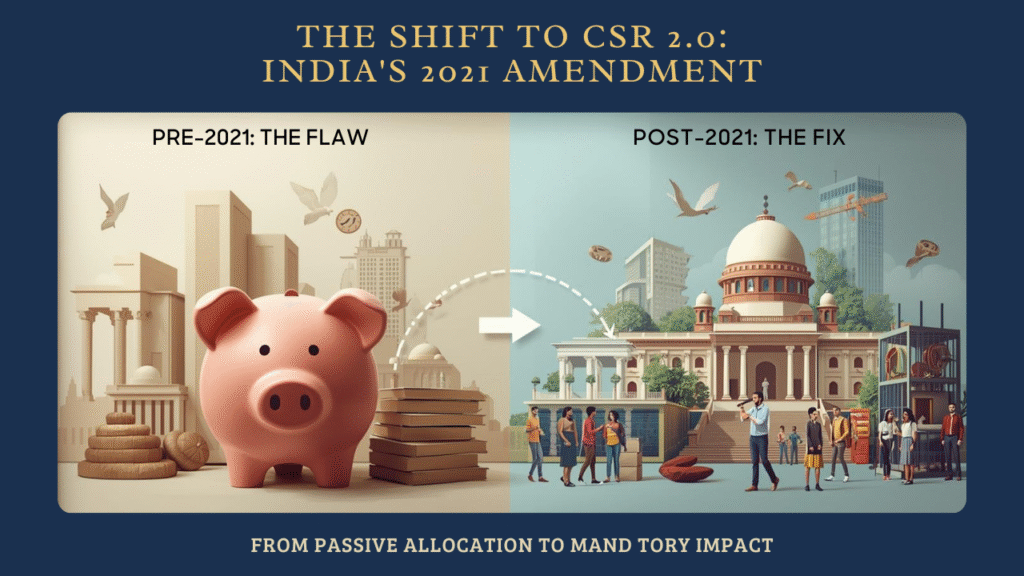

5. The Shift to CSR 2.0: How India’s 2021 Amendment Changed Corporate Accountability

5.1 Understanding the Pre-2021 CSR Challenge

Before 2021, India’s Corporate Social Responsibility (CSR) rules had a fundamental flaw: companies could meet their legal duty just by allocating the money, and not spending it.

This made the law feel like a ‘box-ticking’ exercise. Funds meant for social good simply sat in bank accounts, gathering interest instead of creating impact. Checking a ledger book overshadowed the entire purpose.

The fix started with the Companies (Amendment) Act, 2019. This was the government saying, “Enough is enough.” It introduced real teeth: heavy penalties and the game-changing requirement to transfer unspent funds to a government account within a specific time. This killed the passive ‘hoarding’ model.

The transformation was fully cemented with the Companies (CSR Policy) Amendment Rules, 2021.

These two acts fundamentally changed the system. The gentle “comply or explain why you didn’t” framework was replaced by a firm, non-negotiable “comply or be penalised.”

The net result: CSR became a strict mandate, forcing companies to shift from simply setting aside money to actively deploying it for tangible social impact and real community development.

The Reality of Unspent CSR Funds:

- FY 2022-23: ₹15,787 crore prescribed CSR obligation vs ₹15,602 crore actually spent

- FY 2022-23: ₹1,470 crore unspent, ₹1,643 crore transferred to unspent CSR accounts

- FY 2020-21: ₹1,668 crore sat idle in corporate accounts (7% of obligations)

Why This Gap Mattered: Companies could indefinitely park unspent CSR funds in general accounts with no timeline for deployment. This meant thousands of crores earmarked for social development generated zero impact. There was little incentive to identify quality implementation partners or develop meaningful programs. The mandate’s original purpose, channelling corporate wealth toward India’s development challenges, was being undermined by a critical loophole.

5.2 The 2021 Amendment: Three Game-Changing Reforms

The January 2021 amendments to the Companies Act, by the Parliament, redefined CSR from a spending exercise into an accountability-driven framework.

5.2.1. Mandatory Unspent CSR Account

The new rules have completely killed the loophole that let companies park their CSR money!

Here’s the deal now:

If you have unspent CSR funds, you can’t just let them sit there. You must transfer that money to a special, separate account within six months of the end of the year.

For money meant for ongoing projects, you get a three-year window to use it. If it remains unused after those three years, it must be surrendered; it goes straight to a government-specified pot, like the Prime Minister’s Relief Fund or other Schedule VII funds.

In short, the money has to be spent on social good, or it goes to the state. There’s no legal way to store it anymore.

5.2.2. Impact Assessment Requirement

Companies with CSR obligations of ₹10 crore or more must conduct independent impact assessments through third-party agencies for projects worth ₹1 crore or above. Companies can allocate up to 5% of total CSR spending or ₹50 lakh (whichever is lower) toward these assessments.

The shift is profound: companies must now measure outcomes, not just outputs. It’s no longer sufficient to report “1,000 people trained”; you must demonstrate “employment rates increased by X%” or “incomes rose by Y%.”

5.2.3. Strengthened Penalties

This amendment introduced not just fines, but stiffer penalties and the threat of disqualifying directors if companies didn’t comply.

This instantly turned CSR from a simple administrative task handled lower down a corporate “afterthought” into a critical, strategic priority that lands squarely on the Board’s table. Now, non-compliance has high stakes, forcing senior leadership to take genuine accountability for social spending.

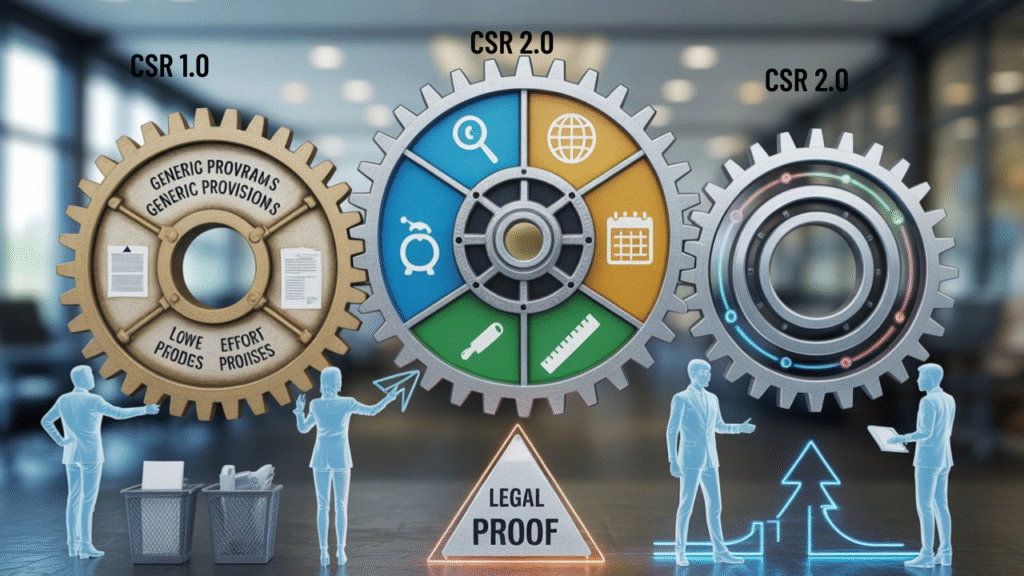

5.3 CSR 2.0: The Evolution from Spending to Impact

CSR 2.0 is a complete change in how companies think. It moves the goalposts from simply hitting a percentage spending target to genuinely creating systemic, measurable, and lasting change in society.

It’s the crucial difference between merely writing a check (corporate philanthropy) and undertaking thoughtful, long-term initiatives that yield real returns for communities (strategic social investment). The focus is now on impact, not just intent.

5.3.1 Key Differences: CSR 1.0 vs. CSR 2.0

| Old Way – CSR 1.0 (up to 2021) | New Way – CSR 2.0 (after 2021) |

| Focus on spending the 2% threshold | Focus on measuring outcomes and impact |

| The goal was simply to hit the 2% number, just making sure the required budget was spent. | The goal is actual results proving that the money made a real difference and creating a lasting impact. |

| Fragmented, one-off projects | Systemic, multi-year programs with clear theories of change |

| Random, one-time projects done, such as giving a donation and walking away. | Thoughtful, long-term programs with a clear plan for how and why they will solve a specific problem. |

| Minimal accountability or tracking | Mandatory impact assessments and third-party audits |

| Spending was often tracked internally with little oversight, a black box. | Spending must now be validated externally through audits and proof of impact to ensure honesty. |

| Safe, easy-to-execute activities (awareness campaigns, one-time donations) | Complex, high-impact interventions addressing root causes |

| Sticking to simple, low-risk actions that look good on paper but don’t challenge the issue. | Taking on tougher, deeper challenges that address why the problem exists, not just its symptoms. |

| Geographic concentration in metro areas | Push toward equitable distribution in underserved regions |

| Putting the money in easy-to-reach, urban areas. | A mandated shift to serve the most needy areas and ensure funds reach neglected, rural communities. |

| Siloed from core business strategy | Integrated with ESG frameworks and corporate purpose |

| CSR was treated as a separate, side department with no connection to the company’s main work. | CSR is now woven into the company’s DNA, connecting social efforts to environmental goals and core business values. |

| Output-based reporting (“X schools built”) | Outcome-based reporting (“Y% improvement in learning outcomes”) |

| Reporting on easy activity counts what you built or bought. | Reporting on real-world change, the actual improvements or benefits achieved because of your project. |

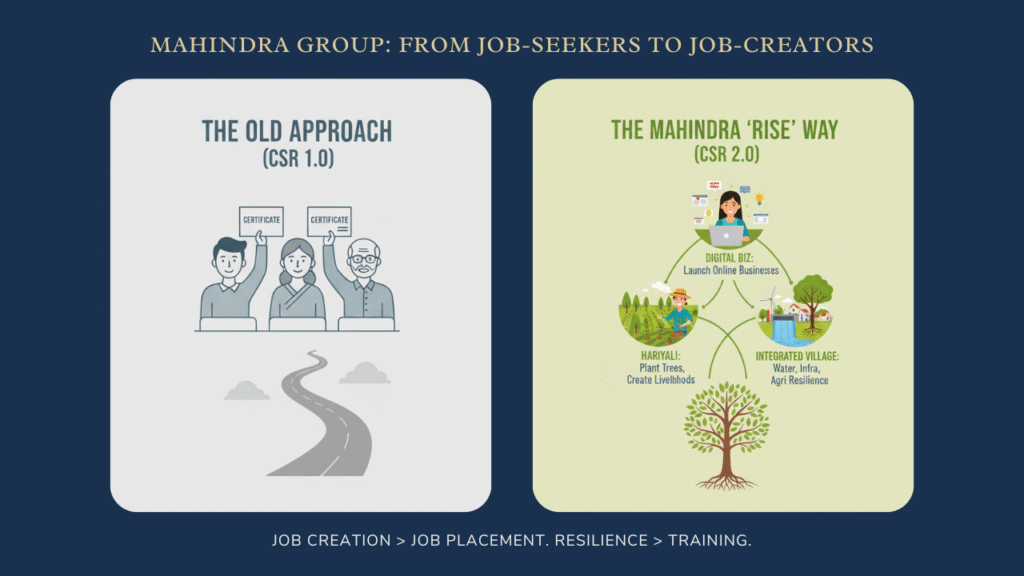

5.4 Mahindra Group: From Job-Seekers to Job-Creators

he Old Approach: Train People, Hope for the Best

Most companies run skill development programs that end with a certificate. Participants learn a trade, get their paperwork, and then… what? Finding employment becomes their problem.

The Mahindra “Rise” Way: Build Sustainable Livelihoods

Mahindra’s “Rise” initiative flipped the script entirely. Instead of creating people who need jobs, they focus on creating people who create jobs, entrepreneurs, not employees.

What This Looks Like in Practice:

- Digital literacy programs that go beyond teaching women basic computer skills help them start and run their own online businesses

- Regenerative farming initiatives like Hariyali, which have planted over 19 million trees while creating genuine income opportunities for villagers and tribal communities

- Integrated Village Development Programs that address water management, infrastructure, and sustainable agriculture all at once, tackling root causes rather than just surface-level problems

The distinction matters. When you teach someone to farm sustainably, they don’t just feed their family better; they reduce costs, improve soil health, and create economic resilience that lasts generations.

Why This Is CSR 2.0: Job creation over job placement. Economic resilience over one-time training. Sustainable livelihoods over temporary solutions.

5.5 Why This Matters for India’s Development

The shift to CSR 2.0 brings real change across the board:

For Companies: CSR isn’t just about ticking boxes anymore; it’s become core to how businesses handle risk, connect with stakeholders, and create real long-term value. Boards need to give social investments the same serious attention they give to financial decisions.

For Communities: The quality of interventions improves dramatically, leading to deeper and more sustainable impact. Communities aren’t getting scattered one-time projects anymore; they’re seeing multi-year commitments that can genuinely transform education systems, healthcare access, livelihoods, and environmental conditions.

For India’s Development Goals: An outcomes-focused CSR directly supports achieving the Sustainable Development Goals by 2030. With stronger measurement and accountability, resources are genuinely addressing poverty, education gaps, health crises, and climate issues rather than just being allocated and forgotten.

5.6 What Makes CSR 2.0 Different: The Accountability Factor

The 2021 amendments did way more than just create extra paperwork; they fundamentally shifted how companies behave. When you have to prove impact through independent assessments, you can’t get away with generic, low-effort programs anymore. You actually need:

- Clear baseline data and monitoring systems

- Partnerships with credible organisations that can execute

- Multi-year commitments to see meaningful change

- Real investment in measurement and evaluation capacity.

That’s why we’re watching companies shift from “CSR as compliance” to “CSR as strategic investment” because the law now demands proof, not just promises.

Key Takeaways:

- The 2021 amendment closed critical loopholes around unspent funds and the lack of accountability

- Impact assessment requirements force outcome-focused program design

- CSR 2.0 represents an evolution from quantitative compliance to qualitative impact

- Leading companies are integrating CSR with ESG strategy and core business operations

- The focus has shifted from spending percentages to creating measurable, sustainable social change

6. CSR 3.0: The Future is ESG Integration and Tech-Driven Impact

6.1 What is CSR 3.0?

CSR 3.0 is the complete strategic fusion of Corporate Social Responsibility and ESG (Environmental, Social, and Governance) principles. It signifies a shift from mere compliance to core business integration, where social impact is:

- Quantified: Measured by AI-driven SROI (Social Return on Investment), treating social capital as a balance sheet asset.

- Integrated: Governed by a holistic Triple Bottom Line (People, Planet, Profit) framework.

- Essential: Indistinguishable from core business operations, a fundamental driver of long-term profitability and risk management.

CSR 3.0 is when a company realizes that doing good is simply how you do business. It’s the shift from being a company that reports on its environmental footprint to one where your core product or service actually solves a social or environmental problem.

Instead of seeing investment in community and employee well-being as a “cost,” CSR 3.0 sees it as social capital, a measurable asset that secures long-term loyalty, reduces risk, and drives innovation.

6.2 The Technology Revolution: AI, Data, and Blockchain

Technology is making everything more transparent and efficient:

- AI-Driven Impact Measurement: Uses predictive analytics to figure out which interventions will have the biggest impact and image recognition to verify projects remotely.

- Blockchain for Transparency: Makes sure funds can be traced, tracking every rupee from the corporate account all the way to the final beneficiary to prevent fraud.

6.3 Criticisms That Remain

The next decade’s challenges include:

- The Employment Gap: CSR pours money into skill development but avoids the harder problem of actually creating jobs.

- The Innovation Deficit: Over-reliance on “safe” sectors kills investment in high-risk, high-reward areas like climate tech, mental health, and disability inclusion.

- SME Exclusion: The ₹5 crore profit threshold shuts out lakhs of MSMEs that collectively represent significant resources.

6.4 Strategic Leadership: CSR 3.0 Case Studies & Best Practices in India

Leading Indian companies demonstrate responsible business practices by strategically fusing social impact with core business, leveraging ESG goals for competitive advantage:

| Company | Strategic CSR 3.0 Initiative | Link to CSR 3.0 Principle |

| Tata Chemicals | Sustainable Livelihood Focus: Strategic investment in the Self-Reliant Rural Development initiative that trains farmers in organic, high-yield agriculture. This lifts local incomes (People) while securing their agricultural supply chain (Profit). | Integrated & Essential: Links supply chain stability with community well-being. |

| Mahindra Group | Rise” Philosophy & Carbon Neutrality: Focused on sustainable mobility and clean energy. The Group’s goal to reach Carbon Neutrality by 2040 (Planet) and its widespread Skills Development programs (People) are central to its ‘Rise’ purpose and brand value. | Essential & Triple Bottom Line: Sustainability drives brand value, innovation, and financial resilience. |

| Infosys Foundation | High-Impact Societal Digitalisation: Infosys leverages its tech expertise for real societal impact, rolling out large-scale digital literacy and e-governance programs that put its core IT competency to work solving systemic challenges. | Quantified & Integrated: Using core business IP to create measurable social capital. |

6.5 Critical Challenges Still Holding Back Indian CSR

Despite progress, Indian CSR efforts often miss the mark by focusing on easy wins instead of deep, strategic impact.

- The Employment Gap: Companies dump money into skill enhancement (easy to report!), but completely skip the harder problem: job creation. The result? Lots of trained youth, but no actual jobs. ($$ to Training ≠ Jobs)

- Geographic Inequality: Too much money clusters in a few rich, urban states. 62% of funds concentrate in hotspots like Maharashtra and Karnataka. Poor, rural areas that need the investment most often get left behind.

- Innovation Deficit: Companies play it safe, sticking to familiar territory like building classrooms or organising basic health camps. This means newer, more challenging areas like climate technology, genuine mental health support, or disability inclusion struggle to get funding. Everyone’s afraid to take big bets on solutions that could actually transform lives.

- SME Exclusion: The ₹5 crore profit threshold excludes thousands of SMEs (Small and Medium Enterprises) from the formal CSR framework. These local businesses, which collectively represent a massive resource, are unable to contribute to the national CSR pool despite their potential impact.

The CSR 3.0 Solution? Shift from a compliance mindset to a strategic one. The future demands funding projects that create sustainable markets (Entrepreneurship), demand transparency (Tech-Driven), and tackle tomorrow’s biggest threats (Innovation/ESG)

7. Conclusion: India’s CSR From Obligation to Opportunity

CSR in India has moved way beyond simple charity; it’s about shifting from the ₹5 crore legal mandate to a billion-dollar mindset for change.

Companies have evolved from sporadic philanthropy (CSR 1.0) to rigid compliance (CSR 2.0). But the critical challenges that remain are severe geographic inequality and the innovation deficit in spending, which show that true integration is still the next frontier.

The future demands a decisive leap into Strategic CSR (CSR 3.0):

- The Goal is Impact: Stop treating the 2% as a minimum spending requirement to report, and start seeing it as an impact investment that solves systemic problems.

- The Focus is Alignment: Shift CSR funds out of comfortable urban areas and into Aspirational Districts, directing spending toward the nation’s greatest needs rather than just areas convenient to corporate headquarters.

- The Strategy is Innovation: Break away from “safe” sectors like basic education and health to champion high-risk, high-reward areas like climate tech, mental health, and inclusive livelihood creation.

Ultimately, for Indian CSR to realise its potential, it needs to shift from being an isolated department focused on reporting outputs to an integrated business function focused on creating sustainable social and economic value for all stakeholders. This is a complex transition that requires specialised tools and dedicated guidance.

As the Co-Founder of RELIFC, a platform dedicated to maximising the efficiency of social impact investments, I believe the core challenge is making strategic decisions based on real-time needs, not tradition. The companies that succeed in CSR 3.0 will be the ones that use technology to ensure every rupee spent directly addresses a verifiable development gap. This is the path to real and shared prosperity.FAQS

1. How is CSR evolving in India?

CSR is moving beyond just social spending into full ESG integration. When the 2013 law came in, it focused on the social side, but today the market wants complete accountability. CSR 3.0 is about companies connecting their mandatory CSR work with their overall Environmental, Social, and Governance strategy to manage risks better and create lasting value for all stakeholders.

2. Who is the founder of CSR in India?

Jamshedji Nusserwanji Tata is considered the pioneer who institutionalised CSR in India through the Tata Group’s 150-year legacy of social welfare. However, Mahatma Gandhi laid the philosophical foundation with his Trusteeship Model in the 1940s, which made him the father of CSR philosophy in India. So Tata showed how to practice it, while Gandhi provided the ideology behind it.

3. What is the scope of corporate social responsibility under Indian law?

Under Schedule VII of the Companies Act 2013, CSR scope includes poverty alleviation, education, healthcare, environmental sustainability, rural development, gender equality, disaster relief, and support for armed forces veterans. The 2021 amendment expanded this to include COVID-19 relief and the welfare of migrant workers, broadening the areas where companies can direct their CSR spending.

4. What is the minimum profit required for a company to be mandated to spend on CSR in India?

A company needs to spend on CSR if it hits any of these marks in the previous financial year: net profit of ₹5 crore or more, OR net worth of ₹500 crore or more, OR turnover of ₹1,000 crore or more. Once you qualify, you’re required to spend 2% of your average net profit from the last three years.

5. What happens if a company fails to spend the mandatory 2% CSR amount?

The 2021 Amendment tightened things up considerably. If you have unspent funds tied to ongoing projects, you’ve got six months to move them into a special Unspent CSR Account, then three years to actually use them. For projects that aren’t ongoing, those funds go straight to a Schedule VII fund like the PM Relief Fund. Companies and their directors who don’t follow these rules face serious fines and penalties.

6. What is Schedule VII of the Companies Act, 2013?

Schedule VII is the official menu of where CSR money can go. It includes all the major social areas, things like poverty reduction, better schools and hospitals, environmental work, rural development, and disaster response. During COVID, the government added pandemic relief to this list so companies could use their CSR funds to help during that crisis.